Portfolio construction is crucial and, in our view, its importance is at times underappreciated. As we wrote in the Evanston Capital 2026 Hedge Fund Outlook, “in this environment, we believe portfolio construction has evolved to become an even more valuable source of edge.”

Brendan James, CFA, an Evanston Capital partner and a member of our Investment Team, is the lead author of a new series discussing portfolio construction theory and how assets ultimately fit together in building our portfolios. The series consists of three parts:

Part I — The Diversification Sweet Spot

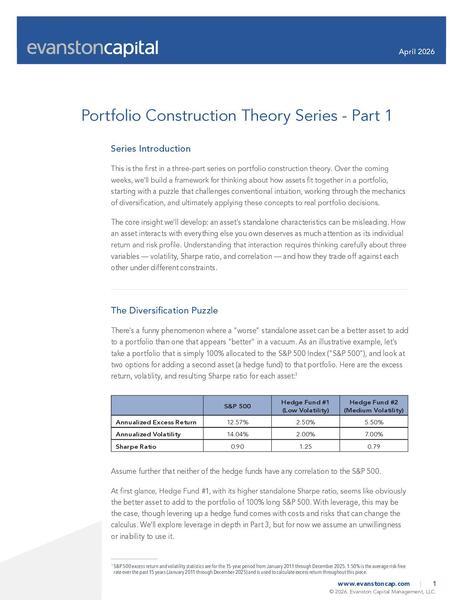

Here, we begin building a framework for thinking about how assets fit together in a portfolio, starting with a puzzle that challenges conventional intuition, working through the mechanics of diversification, and ultimately applying these concepts to real portfolio decisions.

The core insight we’ll develop: an asset’s standalone characteristics can be misleading. How an asset interacts with everything else you own deserves as much attention as its individual return and risk profile.

In this first entry in the series, we establish that diversification benefit is maximized when assets contribute equal risk to the portfolio, which we call the “Diversification Sweet Spot.”

Part II — Sharpe Ratio and Correlation

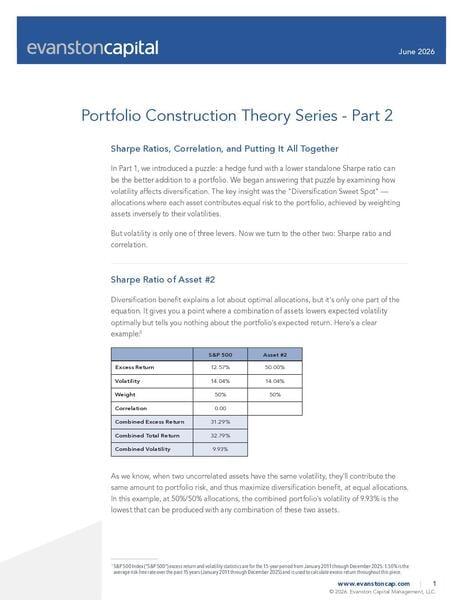

Having introduced and resolved a puzzle — a hedge fund with a lower standalone Sharpe ratio can be the better addition to a portfolio — we now turn from volatility to the other two levers: Sharpe ratio and correlation.

We thereby complete the theoretical framework:

- Volatility determines the diversification sweet spot;

- Sharpe ratio differences pull you toward stronger risk/reward assets; and

- Correlation determines how much diversification benefit is available to offset Sharpe differences.

Part III — Constrained Optimization and the Case for (or Against) Leverage

In Parts 1 and 2, we built a framework for thinking about how assets combine in a portfolio. We established that diversification benefit is maximized at the “Diversification Sweet Spot,” where assets contribute equal risk, and that Sharpe ratio differences and correlation levels determine how far optimal allocations deviate from that point.

Now we apply this framework to the way investors actually make decisions. Most investors can’t simply maximize Sharpe ratio unconstrained. They face a volatility ceiling that can’t be exceeded, or a return floor that must be met.

The key insight is to apply these concepts somewhat in reverse.

The statements made herein may constitute forward-looking statements. These statements reflect EC’s subjective views about, among other things, investment theory, and results may differ, possibly materially, from these statements. These statements are solely for informational purposes, and are subject to change in EC’s sole discretion without notice.

Other similar articles

Adam Blitz on the Fiftyfaces Podcast

March 2026

Hear Evanston Capital's Co-CIO Blitz approach to identifying investment talent, and the consistent philosophy that has shaped Evanston Capital since its founding.

Listen to Podcast

Kristen VanGelder on the Fiftyfaces Podcast

August 2025

Hear Evanston Capital's Co-CIO VanGelder discuss the alpha-generating opportunities in an environment that’s ‘ripe for change.’

Listen to Podcast

Blockchain Market Outlook: What Happens Now That the [Latest] Crypto Bull Market Is Over?

February 2023

While we think the 2022 crypto bear market created short-term turmoil, we think there may be silver linings for the blockchain ecosystem.

Read Article